One of the most frequently asked questions about reverse mortgages is, “How does it differ from a traditional mortgage?”

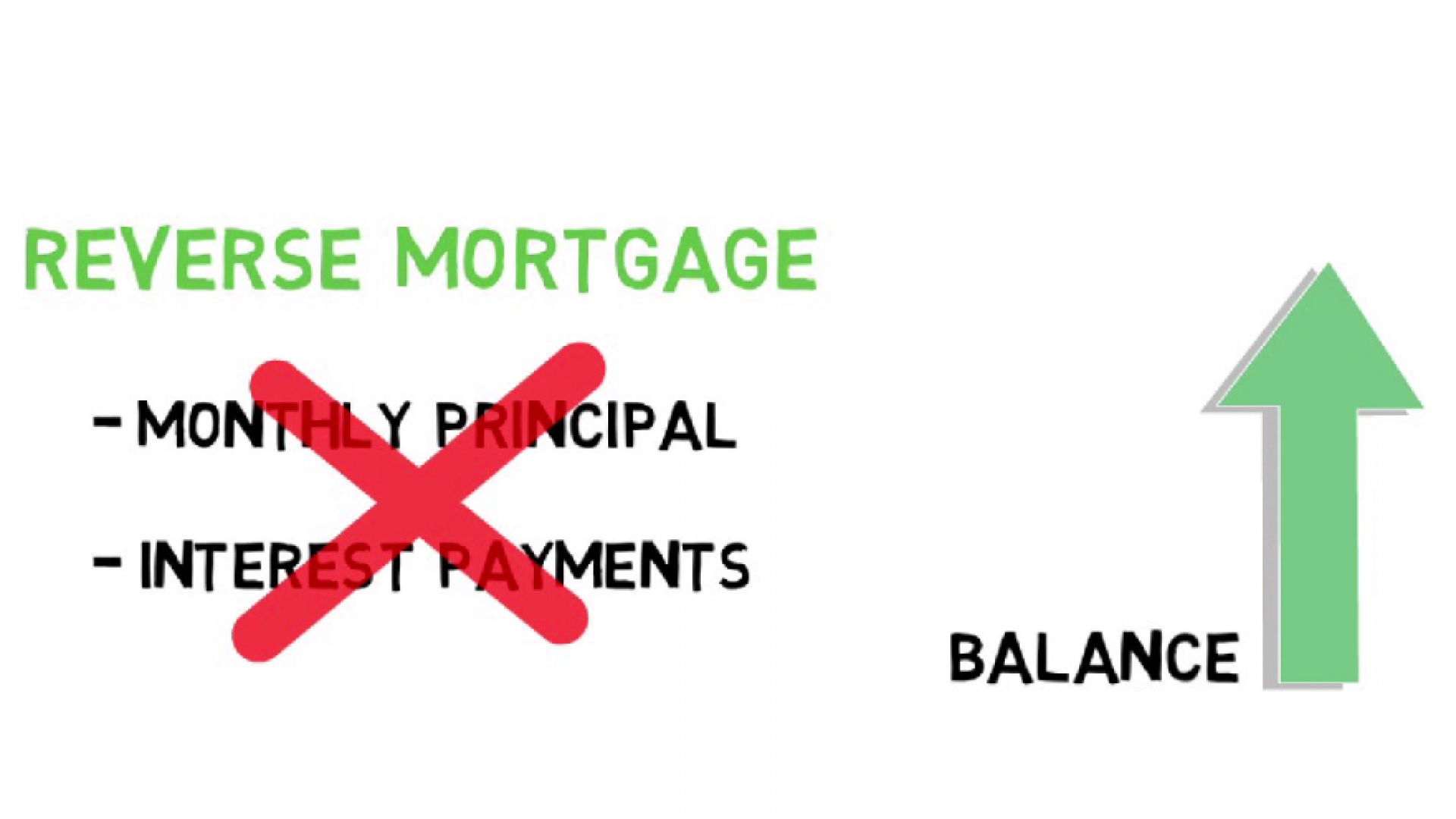

With a traditional mortgage, you make your payments each month, slowly chipping away at the loan balance a little bit at a time. But with a reverse mortgage, monthly principal and interest payments are not required, so the balance goes up over time.

To better understand how a reverse mortgage works, let’s look at a typical scenario. Bob takes out a reverse mortgage for 50% or less of the value of his home, and in the process gains home appreciation averaging 3-4%. That means that his home equity is increasing … even though he’s not making monthly principal and interest payments. The value of his home may be growing faster than his loan balance… turning home equity into retirement cash flow for Bob to use to help fund his retirement while still allowing him to leave a family legacy to his heirs. He can use those funds to renovate his home, fund a grandchild’s education, purchase a new car, or improve his retirement lifestyle.

To find out more about how a reverse mortgage can benefit you and your family, call us today.